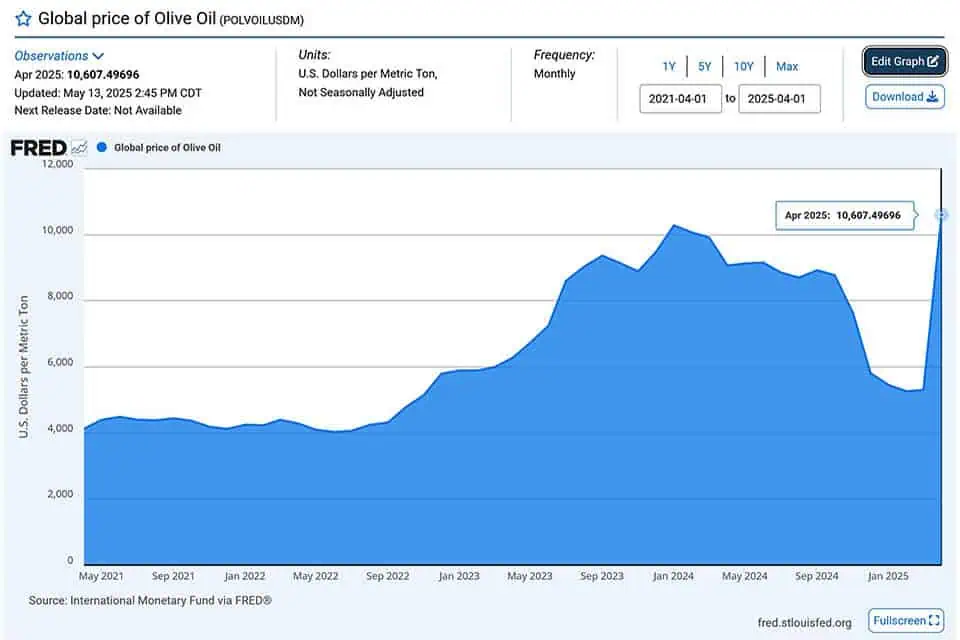

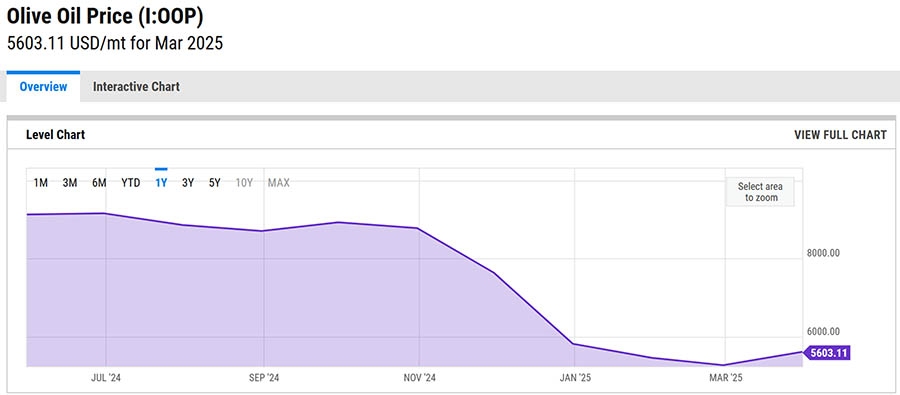

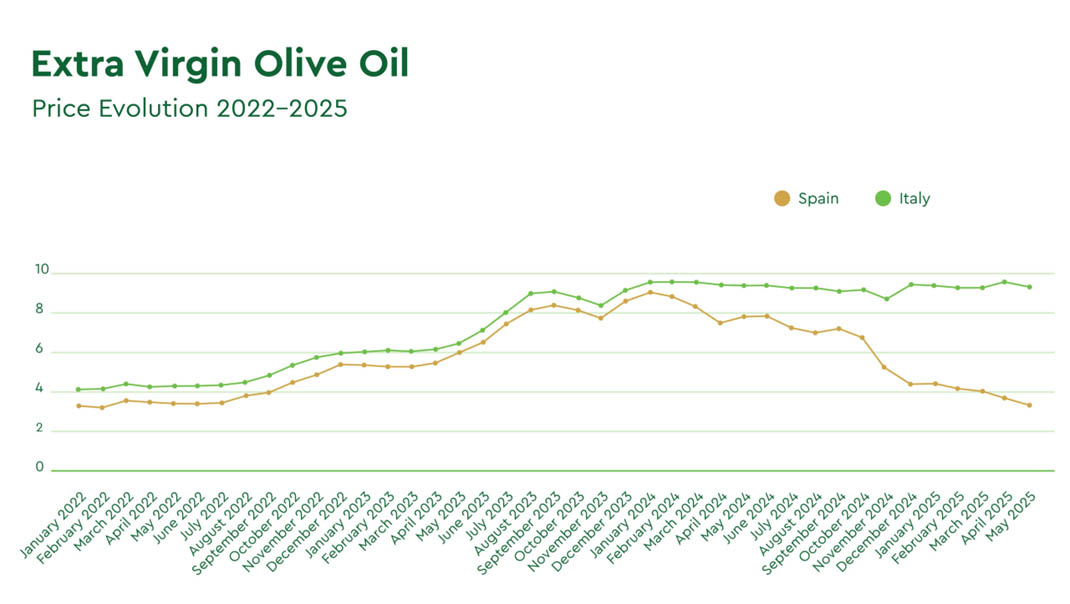

Olive Oil prices in 2025 – the reasons why the olive oil prices dropped

ЦРИТИДА БИО КРЕТСКО МАСЛИНОВО УЉЕ - Произвођачи врхунских критских кулинарских производа: Наши прехрамбени производи се ИЗВОЗЕ ШИРОМ СВЕТА у 40+ земаља, од 1998. - Придружите нам се!

Ми смо вековима дуга породична компанија (1912) која се бави производњом ЕВОО маслиновог уља на острву КРИТ у ГРЧКОЈ. Наше врхунско критско екстра девичанско маслиново уље и кулинарски прехрамбени производи извозе се у више од 40 земаља широм света кроз пажљиво одабрану мрежу партнера. КОНТАКТИРАЈТЕ НАС, БУДИТЕ НАШ СЛЕДЕЋИ ПОСЛОВНИ ПАРТНЕР! за екстра дјевичанско маслиново уље (ЕВОО) - органско (био) екстра дјевичанско маслиново уље (органско ЕВОО) - грчке столне маслине - балзамико сирће - деликатесе, све са КРИТА ГРЧКА

Повезани постови

Цритида Био Критско маслиново уље на ФООДЕКСПО Грееце 2023

Наша компанија ЦРИТИДА БИО КРЕТАН ОЛИВЕ ОИЛ учествоваће на „Фоодекпо Грееце 2023”

Цритида Био Цретан маслиново уље на сајму Фоод Екпо Атхенс Грееце 2022

Цритида Био Цретан Оливе Оил учествоваће на сајму Атхенс Фоод Екпо Грееце 2022.

Зашто је Грчка реч када је у питању маслиново уље – грчки је најбољи ЕВОО на свету

Како доћи до грчког: Зашто је Грчка реч када је у питању маслиново уље (ИЗВОР: Тхе Индепендент УК

Како користити маслиново уље за негу косе – предности

Употреба маслиновог уља за негу косе Маслиново уље за негу косе: Како користити и могуће користи Маслиново уље и